Refinancing can be a smart way to adjust your mortgage to fit your current needs. Whether you’re looking to lower your monthly payment, shorten your loan term, or free up room in your budget, the right refinance could help you reach your goals.

Refinancing replaces your current mortgage with a new one that is a better fit. For many homeowners, that means securing a lower interest rate and reducing their monthly payment. Even a small drop in your rate can make a meaningful difference over time, freeing up cash for savings, home improvements, or everyday expenses.

But refinancing isn’t one-size-fits-all, and that’s where working with the right team matters. Sentinel FCU takes the time to understand your goals whether that’s lowering your payment, shortening your loan term, or tapping into your home’s equity. For some, refinancing into a shorter-term loan can mean paying off their home years sooner and saving significantly on interest. For others, a cash-out refinance can provide funds for renovations, debt consolidation, or other major life expenses.

Another reason to consider refinancing is stability. If you currently have an adjustable-rate mortgage, moving into a fixed-rate loan can provide predictability and peace of mind, especially in a changing rate environment.

What sets the Sentinel FCU Team apart is our approach. We don’t believe in pushing a refinance just because it’s available, we focus on whether it benefits you. Our team walks you through every step, explains your options clearly, and provides transparent estimates so you can make an informed decision with confidence. We also offer a variety of loan programs and low down payment options, ensuring we can tailor solutions that fit your financial situation.

Refinancing should feel like a step forward, not a guessing game. If you’ve been wondering whether it’s the right time or the right move, we’re here to help you run the numbers and explore your options with no pressure, just guidance.

Ultimately, refinancing is about finding a mortgage solution that better fits your needs and helps you work toward your financial goals.

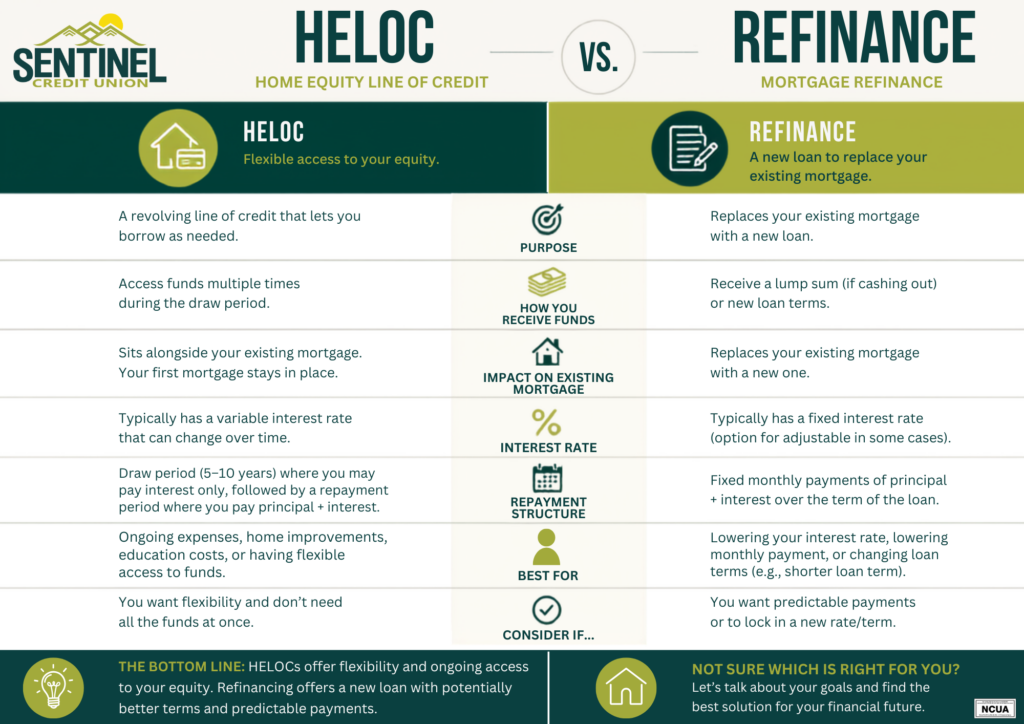

A Home Equity Line of Credit, or HELOC, is often mentioned alongside refinancing, but the two serve very different purposes. Understanding how a HELOC works (and how it differs from other options like a cash-out refinance or home equity loan) can help you decide which path makes the most sense for your goals.

At a high level, a HELOC is a revolving line of credit that uses your home’s equity as collateral. Instead of replacing your current mortgage, like a refinance does, a HELOC sits alongside it as a separate account. Think of it more like a credit card secured by your home you’re approved for a certain limit, and you can draw from it as needed, pay it back, and borrow again during the draw period.

This flexibility is one of the biggest differences. With a cash-out refinance, you receive a lump sum upfront, and your existing mortgage is replaced with a new loan often with a new rate and term. A HELOC, on the other hand, allows you to access funds over time, which can be especially helpful for ongoing projects like home renovations, covering education expenses, or having a financial cushion for unexpected costs.

Another key difference is how interest rates work. HELOCs typically have variable rates, meaning your payment can change over time as market conditions shift. A refinance or traditional home equity loan often comes with a fixed rate, providing more predictable monthly payments. Depending on your comfort level with changing rates, this can be either a benefit or a drawback.

There’s also a difference in how you repay what you borrow. Most HELOCs have a draw period, often around 5 to 10 years, where you can borrow and may only be required to make interest payments. After that, the repayment period begins, where you’ll pay back both principal and interest. This structure can keep payments lower in the short term, but it’s important to plan ahead for when repayment kicks in.

A HELOC can be a great fit if you don’t need all your funds at once or want ongoing access to your home’s equity. It can also make sense if your current mortgage rate is low and you don’t want to replace it with a higher one through refinancing.

The biggest takeaway is that a HELOC isn’t “better” or “worse” than refinancing it’s simply a different tool. The right choice depends on your financial goals, how you plan to use the funds, and what kind of payment structure works best for you.

If you’re considering tapping into your home’s equity, it’s worth having a conversation to explore your options. Reach out to the Sentinel FCU Team for guidance for all mortgage and home equity loan options in the Black Hills, so you can choose the solution that truly supports where you’re headed next.